Main Text starts here.

Financial Information

Latest Financial Results and Forecast

Latest Financial Results

Q1 FY2026 Consolidated Financial Results announced on August 7, 2026

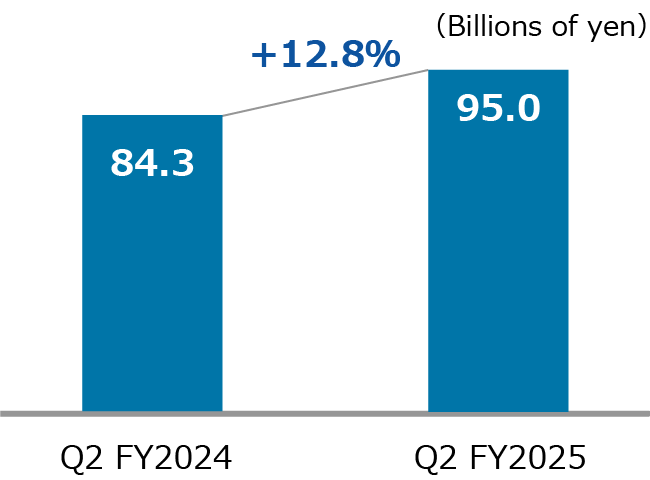

Although there are impacts from a decrease in policies in force, etc., adjusted profit increased by 4.4% year on year to ¥36.6 billion due to the increase in dividends from alternative investments etc.

-

Adjusted profit

[Definition of adjusted profit (to be introduced from FY2024)]

In order to partially adjust for the effect unique to life insurance companies whose net income is reduced in the short term as new policies increase, from FY2024 we introduce “adjusted profit” taking into account the adjustment for the increased burden of regular policy reserves after tax in the first year of new policies.

In addition, We will recognize goodwill from our investment in Daiwa Asset Management Co. Ltd. from Q3 FY2024. The definition of adjusted profit has been revised to add back the amortization of this goodwill.

| Adjusted profit (Source of shareholder return) |

= | Net income (Consolidated) |

+ | Burden of regular policy reserves in the first year | + | Amortization of goodwill |

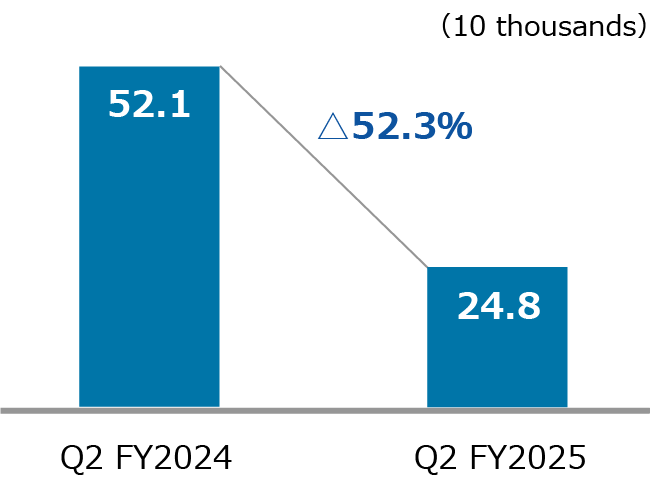

The number of new policies (Individual Insurance) increased by 43.9% year on year to 167 thousand policies due to the insurance premium revision, etc. in May 2026.

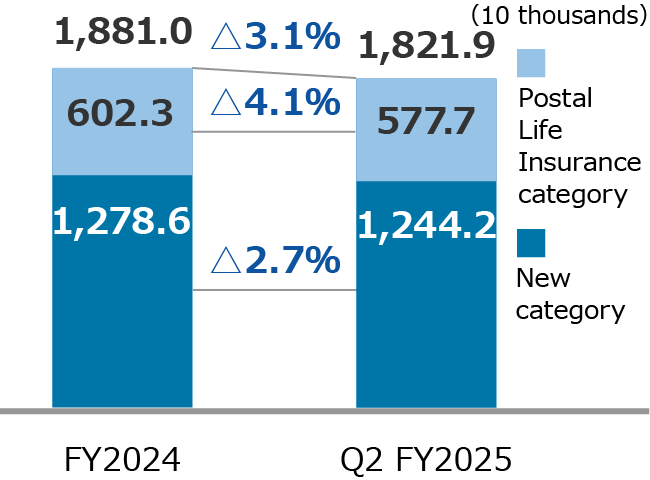

The number of policies in force decreased by 1.0% to 17,547 thousand from the end of the previous fiscal year. By revitalizing sales activities, etc., we continue to aim for a swift turnaround and recovery in the new category*.

-

Number of New Policies

(Individual Insurance)

-

Number of Policies in Force

(Individual Insurance)

- “New category” shows individual insurance policies underwritten by Japan Post Insurance. “Postal Life Insurance category” shows postal life insurance policies reinsured by Japan Post Insurance from Organization for Postal Savings, Postal Life Insurance and Post Office Network.

For details, please check the latest ‘Conference Call Material’ and ’Performance and Financial Data’

Financial Results Forecast

FY2026 Consolidated Financial Results Forecast announced on May 15, 2026

Although there are impacts from a decrease in policies in force, etc., adjusted profit is forecast to be approximately ¥ 155.0 billion, as investment income is expected to remain strong.

Adjusted profit in the three months ended June 30, 2026, reached ¥36.6bn, supported by higher-than-planned dividends from alternative assets, etc.

Although stock dividend income tends to be concentrated in the second and fourth quarters, resulting in a lower first-quarter progress rate due to seasonal factors, progress against the financial results forecast was solid at 23.7%.

(Billions of yen)

| FY2026 (Forecast) |

FY2026 1Q |

Achievement | ||||

|---|---|---|---|---|---|---|

| Ordinary income | 5,130.0 | 1,364.3 | 26.6% | |||

| Ordinary profit | 250.0 | 69.2 | 27.7% | |||

| Net income (Consolidated) |

141.0 | 34.1 | 24.2% | |||

| Adjusted profit | Approx 155.0 | 36.6 | 23.7% | |||

Relate starts here.

IR information