Main Text starts here.

Corporate Information

Business Risks and Other Risk Factors

Business Risks and Other Risk Factors

Disclaimer

This translation does not constitute a solicitation for investments in the stocks and other securities issued by the companies of the Japan Post Group, regardless of whether in Japan or overseas.

UNOFFICIAL TRANSLATION

The following is an English translation of “Business Risks and Other Risk Factors” described in the Annual Securities Report (20th term), which is provided only in Japanese.

Although Japan Post Insurance pays close attention to providing an English translation of the information disclosed in Japanese, the Japanese original prevails over the English translation in the case of any discrepancy.

This text is based on the judgment of the Company and its consolidated subsidiaries (hereinafter referred to as “the Group”) as of the filing date of the 20th Annual Securities Report, unless otherwise stated.

(1) Risk management systems and processes for identifying and managing business risks and other risk factors, etc.

In accordance with the “Basic Risk Management Policy,” we have set up and regularly convene the Risk Management Committee headed by the Chief Risk Officer (CRO), while formulating rules of risk management.

The Risk Management Committee deliberates on risk management policies and matters concerning the establishment and operation of risk management systems as well as on matters concerning the implementation of risk management. This committee also performs appropriate risk management by monitoring and analyzing the status of each risk and other related matters. The CRO submits and reports on important matters to the Executive Committee, the Audit Committee, and the Board of Directors for discussion. (details stated in “IV. Status of Submitting Company, 4. Corporate Governance, etc., (1) Overview of corporate governance, ③ Other matters regarding corporate governance, b. Status of establishment of risk management systems” of the 20th Annual Securities Report).

Among the matters related to business conditions, accounting conditions, etc., described in the 20th Annual Securities Report , business risks and other risk factors are referred to as major risks that management believes may have a significant impact on the Group’s financial position, operating results, cash flow status, and indicators such as EV (embedded value) of corporate value and solvency margin ratio (solvency margin ratio based on economic value) of soundness. The most significant risks and risks recognized to have been increasing in awareness through FY2026 or to increase in awareness in FY2026 are identified after considering the degree of impact and the possibility of the occurrence and managed throughout the fiscal year. In classifying such risks and describing the information related to each one, we conducted a questionnaire (hereinafter referred to as the “Management Questionnaire”) regarding business risks and other risk factors directed at members of the Executive Committee as of March 31, 2026, who were executive officers at or above the level of managing executive officer and those in charge of business operations as of March 31, 2026, in order to appropriately reflect the Company management’s awareness of the impact, possibility of occurrence, and countermeasures. Based on the aggregate results, the Risk Management Committee and the Executive Committee discussed the results and listened to the opinions of Outside Directors. The risk items are also reassessed through the said questionnaire.

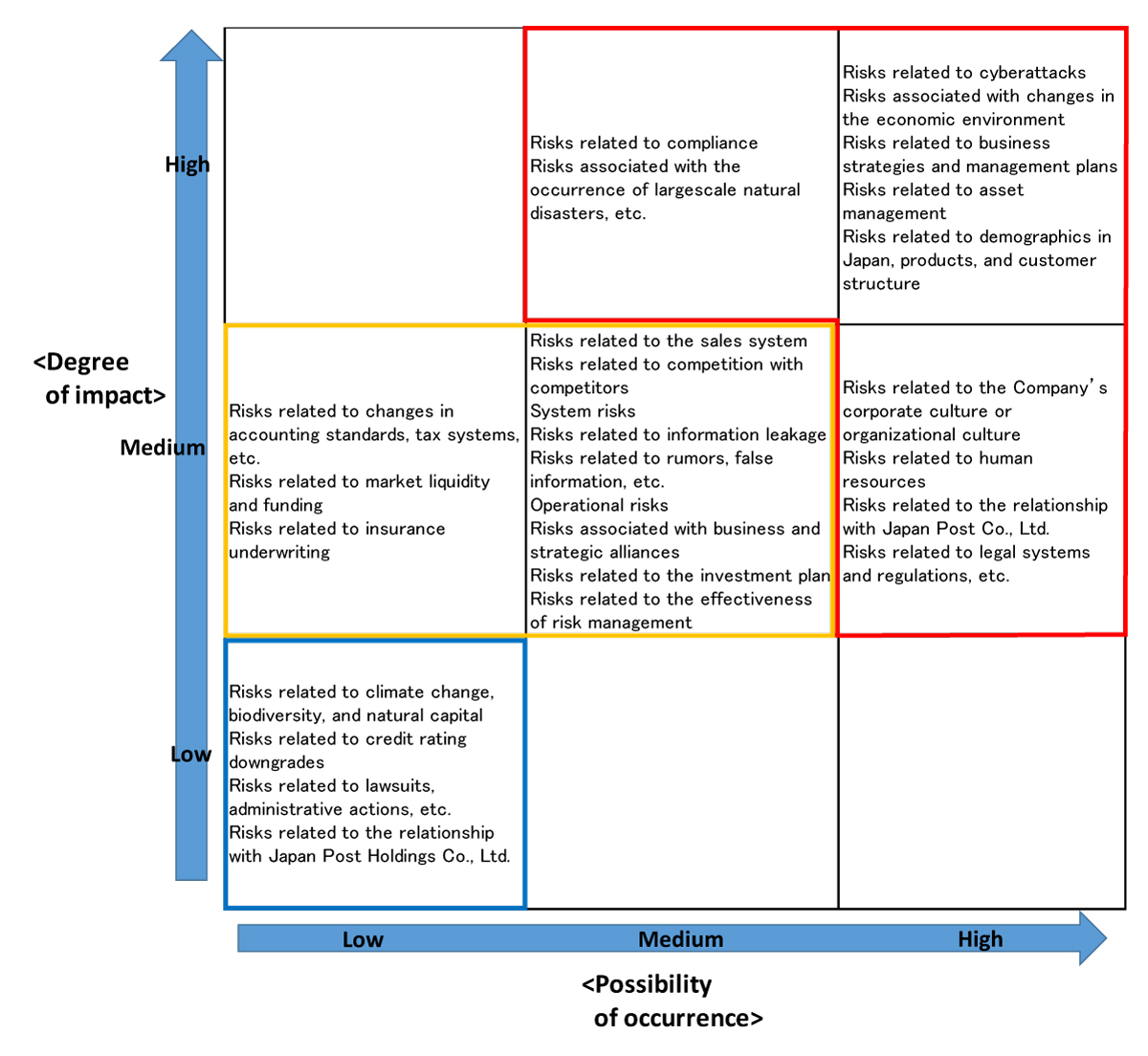

(2) Risk map and most significant risks, etc.

Risk map

The risk map of business risks and other risk factors formulated based on the aggregate results of the Management Questionnaire and in consideration of the impact and possibility of occurrence of risks is as follows.

Most significant risks

Through discussions by the Risk Management Committee based on the Management Questionnaire, the Company has positioned risks with a relatively high impact and high possibility of occurrence, as indicated by the risk map, as the most significant risks for the Company. In FY2026, the business risks and other risk factors selected as the most significant risks are as follows.

| Most significant risks |

|---|

| Risks related to cyberattacks |

| Risks associated with changes in the economic environment |

| Risks related to asset management |

| Risks related to the relationship with Japan Post Co., Ltd. |

| Risks related to compliance |

| Risks related to products and customer structure |

| Risks related to the Company’s corporate culture or organizational culture |

| Risks related to information leakage |

| Risks related to the Insurance Business Act and other related business regulations |

| Risks related to laws and regulations under the Postal Service Privatization Act, etc. |

| Risks related to quality assurance in the insurance solicitation process |

| System risk |

| Risks related to the sales system |

| Risks related to competition with competitors |

| Risks related to human resources |

Risks recognized to have been increasing in awareness through FY2026 or to increase in awareness in FY2026

Business risks and other risk factors selected as risks recognized to have been increasing in awareness through FY2026 or to increase in awareness in FY2026 are as follows.

| Risks recognized to have been increasing in awareness through FY2026 or to increase in awareness in FY2026 |

|---|

| Risks related to cyberattacks |

| Risks related to the Insurance Business Act and other related business regulations |

| Risks associated with changes in the economic environment |

| Risks related to asset management |

| System risk |

| Risks related to customer experience and AI and digital investments |

| Risks related to insurance underwriting |

| Risks related to rumors, false information, etc. |

| Risks associated with business and strategic alliances |

| Risks related to AI |

| Risks related to geopolitical risks and other uncertainties surrounding the socioeconomic environment |

(3) Individual risk items

Each risk item is categorized and described according to its characteristics as I. Management strategies, II. Finance/asset management, III. Business-specific, IV. Operation, and V. Others.

Ⅰ Management strategies

(1) Risks related to business strategies and management plans

-

As described in “II. Business Overview, 1. Management Policy, Management Environment and Issues to be Addressed, etc., (4) Management Strategy and Issues to be Addressed” of the 20th Annual Securities Report, the Group has set forth its vision for 2040 as “An Essential Company that Continually Creates New Value and Delivers Peace of Mind Nationwide” in the Medium-Term Management Plan (FY2026 – FY2028) (hereinafter refer to as the “Medium-Term Plan”), and will pursue the three key strategies during the three-year period from FY2026 to FY2028 of (a) Establishment of the “JPI Value Delivery Model,” (b) Asset Management that Responds to Changes in the Investment Environment, and Resolution of Social Issues, and (c) “Take on the Future” through business transformation leveraging AI and digital technologies, inorganic growth, and other initiatives to expand the value provided. The various risks described in “Business Risks and Other Risk Factors” are inherent in the initiatives included in such business strategies and management plans. In addition, there is a possibility that there will be increased risks or new risks that may hinder the implementation of the above initiatives by the Company in the future. In addition, the business strategies and management plans have been prepared based on a number of assumptions, including general economic conditions such as market interest rates, foreign exchange rates, stock prices, and the business environment, as well as legal systems. However, if these assumptions are not met, or if the business evaluation of each measure is not sufficiently conducted and the results are not commensurate with the investment amount and costs, it may be impossible to achieve the goals of the business strategies and management plans, which may affect the performance and financial position of the Group.

Of the risks inherent in the various initiatives included in the business strategies and management plans and risks related to the assumptions made when formulating these initiatives, those that are particularly important are as follows.

① Risks related to the sales system

There are many customers who have contact with the Company and the Japan Post Group, and they have significant latent insurance needs. We will respond to these needs through our customer-oriented “JPI Value Delivery Model.”

Furthermore, in our sales activities, we will continue to develop our employees and the post office employees of Japan Post Co., Ltd. so that they can propose solutions tailored to customers’ issues based on careful information gathering and understanding of their intentions, customer-oriented product proposals, and clear and easy-to-understand explanations in accordance with the “Kampo Sales Standard,” our code of conduct for insurance sales. In addition, through the Kampo GD System, which comprehensively and quantitatively evaluates not only sales performance but also the solicitation process and after-sales follow-up services, etc., mechanisms to foster consultants and standardize sales activities, and collaborative systems with post offices at branches nationwide, we will continue to focus on strengthening sales capabilities and ensuring a sustainable sales system.

However, if such efforts are not successful in restoring customer trust or sufficiently meeting customer needs, and thus fail to reverse the decline in policies in force, the Group’s business, performance, and financial position may be affected.

-

② Risks related to products and customer structure

Since the mid-1970s, the birth rate in Japan has generally been on a gradual downward trend and is currently among the lowest in the world. The National Institute of Population and Social Security Research estimates that the total population and the population between the ages of 15 and 64 will continue to decline, and we believe this trend is a major factor in the decline in the total amount of life insurance policies in force in Japan. In addition, the Company’s customer base is heavily weighted toward middle-aged and elderly people and women, with a relatively low proportion of young and working-age customers.

The products we handle include a high proportion of life insurance for individuals, especially savings-type products such as endowment and whole life insurance. In addition to the aforementioned long-term demographic trends in Japan and other factors, the level of domestic employment and household income, savings and investment stance, trends with interest rates and other domestic financial market indicators, the relative attractiveness of other alternative products, and the financial soundness and social trust of insurance companies are affecting the number of new policies and the termination rate of policies in force.

The company is working to understand the various needs of customers of all ages, including young and working age, and to expand our product lineup to respond to their needs, for example, in April 2023, in response to the recent rise in education expenses and requests from customers, we revised Hajime no Kampo, an educational endowment insurance, and in January 2024, began offering lump-sum payment whole life insurance, Tsunagu Shiawase, to meet the needs of middle-aged and elderly customers for lifetime death benefits. In addition, in light of the rise in domestic interest rates, we have revised the assumed interest rates for lump-sum payment whole life insurance in July 2025 and January 2026, and revised the assumed interest rates for basic policies and riders excluding lump-sum payment whole life insurance in May 2026. Moreover, under the JPI Value Delivery Model, we are advancing the expansion of easy-to-understand insurance products that respond to the needs of a wide range of customers, including young and working-age customers, while taking into account environmental changes such as rising interest rates and growing needs for asset formation. However, if the Company’s products and services are unable to respond in a timely manner to the diversification of customer needs or changes in preferences for and access to financial products, the Group’s business, performance, and financial position may be affected.

-

③ Risks related to competition with competitors

The Company faces intense competition in the Japanese life insurance market from domestic life insurance companies, foreign life insurance companies, and various cooperative associations, and recently some of these companies have gained an advantage over the Company with respect to product content and lineup, sales channels and methods, and insurance premium levels. With insurance companies established in the form of a joint-stock company and in the form of a mutual company coexisting and competing, there is a possibility that competitors will become more competitive in the future through consolidation and restructuring with eyes focused on overseas insurance and asset management markets, alliances with other industries, or the development and improvement of attractive products and services, as well as sales channels and methods based on new technologies (generative AI, etc.). Furthermore, if we expand the scope of our business, or if the market structure changes due to factors surrounding the Company such as deregulation or new entrants into the market, new competitive relationships may emerge with companies with which we currently have no competitive relationship. In this manner, competition with competitors may affect the Group’s business, performance, and financial position.

-

④ Risks related to customer experience and AI and digital investments

The Company has worked on a business model that places customer experience (hereinafter referred to as “CX”) as its foremost priority, and advanced the utilization of AI and digital technologies. Furthermore, we have also been working to utilize AI to strengthen our ability to respond to customers and improve operational efficiency in light of the remarkable progress in AI technologies, including generative AI, the rapid development and provision of new products and services utilizing AI by other companies, and the rapid advancement of diversification and efficiency improvements in sales methods. In addition, under the Medium-Term Plan, we will focus on realizing enhanced after-sales service and convenient procedures by utilizing customer data, AI, and digital technologies, and on rebuilding our operations with AI as a premise.

Under these initiatives, we will implement business growth strategy investments of approximately 90.0 billion yen by the end of FY2028, the period of the Medium-Term Plan, and work on business restructuring assuming the adoption of AI and digital technologies, a fundamental review of business processes, and productivity improvement through reductions in workloads.

However, if the strengthening of CX through the use of AI and digital technologies, and the improvement of productivity do not proceed as expected, or if AI and other technologies advance beyond the Company’s expectations, resulting in a weakened competitive position relative to other companies, the Group’s business, performance, and financial position may be affected. In addition, these investments will be expensed over the next few years through depreciation, and considerable costs are expected for their management and maintenance. If results commensurate with the investment amount or costs are not achieved, the Group’s performance and financial position may be affected.

-

⑤ Risks related to AI

The utilization of AI may involve compliance risks such as leakage of confidential information and infringement of intellectual property rights such as copyrights, and it is necessary to recognize that there are also significant risks lurking in technical and ethical aspects, such as hallucination in AI outputs, opacity of judgments, and the promotion of bias (prejudice and discrimination) and division. In addition, because the de facto standard for AI has not been established, and given the rapid progress of AI technology, there is a possibility that the technologies adopted by the Company may lose their competitiveness or that new AI technology may pose a threat to existing digital technologies. Furthermore, in Japan, the Act on Promotion of Research and Development, and Utilization of Artificial Intelligence-related Technology (AI Act) came into effect in 2025, and the regulatory environment for AI is being rapidly established; there is also a risk that delays in responding to these regulatory changes may adversely affect the Company’s business development.

If the risks inherent in AI technology materialize (such as disadvantages to customers due to inappropriate use of AI), significant impacts on business may occur, and time and costs will be required for recovery, recurrence prevention, and trust restoration, and the Group’s business, social credibility, performance, and financial position may be affected. Moreover, the emergence of AI risk in the supply chain through third parties such as contractors may similarly cause significant impacts.

Therefore, the Japan Post Group has formulated a Group-wide unified AI policy with the aim of further promoting AI utilization and strengthening the governance system that supports it, and the Company has established rules regarding AI utilization and conducts an advance assessment when introducing AI. We are also progressively establishing the framework so that important risks can be identified and necessary countermeasures can be taken under a company-wide risk management system. However, in spite of such measures, if the Company’s measures do not function due to unknown threats or other reasons, and significant impacts occur on business, the Group’s business, social credibility, performance, and financial position may be affected.

-

⑥ Risks associated with business and strategic alliances

The Group has been involved in multiple alliances and investments in the asset management business and overseas insurance markets up until now to diversify its revenue sources. Specifically, in the asset management business, we have worked to generate revenue through alliances with MITSUI & CO., LTD. in June 2022 and with Daiwa Securities Group in May 2024. As for Daiwa Asset Management Co. Ltd., in which we acquired 20% of the shares in October 2024 and applied the equity method, we have recorded an amount equivalent to goodwill of 31.9 billion yen as of March 31, 2026. In FY2025, we decided to invest in alternative asset management companies through MKAM Co., Ltd., a joint venture with MITSUI & CO., LTD., and Daiwa Asset Management Co. Ltd., as well as in Ashmore Group, a major U.K. asset management company specializing in emerging markets. In addition, as part of our efforts in the insurance market including overseas, we entered into a strategic partnership agreement with KKR & Co. Inc. (hereinafter referred to as “KKR”) and its subsidiary, Global Atlantic Financial Group (hereinafter referred to as “GA” ), and made investments in the reinsurance co-investment vehicle operated by GA in June 2023, and we decided to make an additional investment of approximately USD 2.0 billion in a new reinsurance vehicle in July 2025. Furthermore, in March 2026, as part of the strategic partnership with KKR, we decided to make a minority investment in Hoken Minaoshi Hompo Group.

When entering into alliances with other companies, etc., we execute them upon identifying risks by utilizing outside experts as necessary and establishing the Company’s management system. After entering into alliances, we ascertain the management and financial situations of our partners, etc. and work to prevent risks from materializing, such as by examining the internal controls of investees as necessary.

Going forward, under the strategy to “Take on the Future” set forth in the Medium-Term Plan, we will deepen our existing initiatives while continuously exploring new areas with affinity to the Company’s business, aiming for medium- to long-term growth and improvement in capital efficiency. However, if problems arise in the execution of business or internal controls of partners, etc., or if the business is not conducted as planned, or if the expected results from the partnership, etc. are not achieved, impairment losses may be incurred and the Group’s business, social credibility, performance, and financial position may be affected. In addition, in the event of poor performance in the overseas insurance market or deterioration in the asset management market as the scope of alliances expands overseas, the Group’s business, performance, and financial position may be affected.

-

⑦ Risks related to human resources

In order to conduct its business as a life insurance company, the Group requires talented personnel with a high level of expertise and stable business performance in each field, including insurance sales, actuarial, asset management, and risk management. In particular, with the recent evolution and spread of digital technology (including AI), we recognize that securing and training human resources to promote digital transformation (hereinafter referred to as “DX”) and, given the progression of strategic alliances, etc., human resources with expertise in overseas operations is a pressing issue. Furthermore, as our senior personnel approach mandatory retirement age, expanding and developing our pool of next-generation managers is also vital. However, under the increasing competition for securing human resources mainly due to the impact of the declining birthrate, hiring the quality and quantity of human resources expected by the Company is becoming increasingly challenging. Even if hiring is successful, it may be difficult to retain such human resources. In addition, failure to provide attractive working conditions and workplace environments relative to our competitors, personnel and labor problems such as harassment, as well as health and safety management problems in the workplace may result in an outflow or shortage of human resources.

As stated in “2. Sustainability Philosophy and Initiatives” of the 20th Annual Securities Report, the Group is working to secure and train highly specialized human resources, expand and develop a pool of managers and employees to lead the future of the Company, improve the motivation and satisfaction of our employees, and curb the number of retirements, thereby strengthening human capital management. However, in the event that these efforts are not successful or take longer than expected to be successful, customer service may deteriorate, which could lower the relative competitiveness of the Group or decrease new policies or policies in force, and therefore the Group’s business, performance, and financial position may be affected.

-

⑧ Risks associated with changes in the economic environment

Because most of the revenues of the Group’s businesses are generated in Japan, domestic economic and price conditions, household income trend, savings and investment stance, etc., may affect the businesses conducted by the Group. Furthermore, recent years have given rise to concerns about the impact on the domestic economy of such factors as trends with the trade policies of national governments and conflicts among nations. In this manner, trends in these and other economic and price conditions may affect the Group’s business, performance, and financial position.

Consumer prices are at high levels due to the impact of rising raw materials prices, against a backdrop of continued tight labor supply and demand and pass-through of rising wages to sale prices. If such situations continue beyond our assumptions, concerns will arise about soaring expenses, deterioration in the profitability of insurance premiums from such expenses, difficulty in securing human resources, etc. In addition, if the interest rate level rises more than expected due to the rise in prices, etc., in addition to the emergence of domestic interest rate risk in asset management, cancellation and transfer of policies may increase with policy holders shifting their funds to other financial products to which they can obtain higher returns. Through such a course, the inflation trend in the domestic economy may affect the Group’s business, performance, and financial position.

-

⑨ Risks related to geopolitical risks and other uncertainties surrounding the socioeconomic environment

Recently, uncertainties surrounding the socioeconomic environment are a cause for concern as they may have a serious impact on economic and price conditions and household finances. In particular, geopolitical risks may have a significant impact on economic and price conditions, as in the case of stagflation, and may also cause serious damage to socioeconomic activities themselves, such as difficulties in procuring essential goods. If geopolitical risks or other uncertainties surrounding the socioeconomic environment materialize, the Group’s business, performance, and financial position may be affected.

-

⑩ Risks related to the Company’s corporate culture or organizational culture

In December 2019, the Special Investigation Committee regarding the issues related to the solicitation quality that occurred in FY2019, such as the policy rewriting that disadvantaged customers (hereinafter referred to as the “solicitation quality issues”), consisting of three lawyers who have no vested interest in Japan Post Holdings Co., Ltd., Japan Post Co., Ltd., or the Company, released an investigation report regarding the investigation of the facts and causes of the solicitation quality issues. The report pointed out the existence of a corporate culture or organizational culture in the Group, such as postponing the investigation and resolution of causes when risk events are detected, trivialization of problems, and lack of horizontal cooperation among departments and blocked communication of information under the top-down system. The Group is working to foster a sound corporate culture under the leadership of management, and continues to make steady improvement. However, incidents regarding improper handling of non-public financial information (hereinafter referred to as the “incident involving inappropriate use of non-public financial information) and solicitation of sales of the insurance products such as lump-sum payment whole life insurance before regulatory approval (hereinafter referred to as the “incident involving customer solicitation conducted prior to obtaining regulatory approval” ) have been identified within the Japan Post Group. If initiatives to improve the corporate culture and organizational culture, including measures to prevent recurrence of such incidents, are not successful, or they take longer than expected before they are successful, similar incidents may recur, which may affect the Group’s social credibility, performance, and financial position.

-

⑪ Risks related to credit rating downgrades

The Company has obtained credit ratings from rating agencies and as of March 31, 2026, the Company’s credit ratings were as indicated below. Based on these ratings, the Company believes it has received a favorable evaluation in its financial soundness.

Rating agencies Credit ratings Rating and Investment Information, Inc. (R&I) “AA-” (insurance claims paying ability) Japan Credit Rating Agency, Ltd. (JCR) “AA” (ability to pay insurance claims rating) S&P Global Ratings Japan Inc. (S&P) “A+” (insurer financial strength ratings) Moody’s Japan K.K. (Moody’s) “A1” (insurance financial strength rating) Under the Medium-Term Plan, we will work to stop the decline and begin a rebound in policies in force and to control operating expenses. However, if these efforts do not progress as planned, and if the credit rating of each company is downgraded due to deterioration in the Company’s future financial outlook, the Group may not be able to obtain favorable debt financing in the capital markets, and this may cause uncertainty about the Company, leading to a decrease in new policies and policies in force. In this manner, the Company’s credit ratings from the respective rating agencies may affect the Group’s business, performance, and financial position.

-

⑫ Risks related to climate change, biodiversity, and natural capital

Recognizing the risks and opportunities posed by climate change, the Company expressed its support for the recommendations of the TCFD (Task Force on Climate-related Financial Disclosures) in April 2019, and is further promoting its initiatives up until now related to climate change and enhancing information disclosure (details stated in “2. Basic Concept and Initiatives on Sustainability” of the 20th Annual Securities Report).

Climate change has the potential to affect the Company’s performance and financial position, and the Company conducts scenario analysis to assess its impact.

We recognize that the main impacts of climate change on our life insurance business include possibilities of a rise in insurance claim payment due to increased damage from natural disaster, etc., and a rise in insurance claim payment due to changes in mortality and morbidity rates over the medium to long term due to the impact of rising average temperature and abnormal weather. In addition, as major impacts on asset management, we recognize the risk of impaired value of investment and loan assets due to expanding loss incurred by investees or borrowers upon increased damage from natural disasters, etc., and the risk of impaired value of investees or borrowers due to the impact of changes in regulations in line with the shift to a low-carbon society, stricter regulations and changes in consumer preference.In addition, in order to manage our investment portfolio based on GHG emissions, we measure and analyze GHG emissions of our investment portfolio and, taking into account the analysis results, engage in constructive dialogue (engagement) with investees or borrowers.

Furthermore, with respect to biodiversity and natural capital, which are priority issues on the global level along with climate change, we support the philosophy of the Taskforce on Nature-related Financial Disclosures (TNFD), a global initiative to establish an information disclosure framework related to natural capital. We joined the TNFD Forum to support its activities in June 2023, and in December 2023, we expressed our intention to make disclosure based on TNFD recommendations as an Early Adopter. We are promoting initiatives related to biodiversity and natural capital, and enriching our disclosure of information based on TNFD recommendations.

We recognize the main impact on our life insurance business, including the possibility of a rise in insurance claim payment due to wide spread, etc. of infectious diseases from the collapse of ecological balance as well as the Company’s data centers experiencing operational delays or suspension from various natural disasters.

In terms of asset management, the Company recognizes the risk of impaired value of investment and loan assets due to the depletion of natural capital on which investees or borrowers depend, as well as the risk of impaired value of investment and loan assets due to stricter laws and regulations regarding environmental protection and changes in social demands.

We are conducting analysis on nature-related dependencies and impacts of our investment portfolio, and reflecting its results and consideration for social demands in our asset management activities.

In this manner, we are implementing various initiatives related to climate change, biodiversity, and natural capital; however, if these measures are deemed insufficient, the Group’s reputation in the capital markets and other social evaluation may deteriorate, which may affect the Group’s business, performance, and financial position.

Ⅱ Finance/Asset management

(1) Risks related to insurance underwriting

-

① Risks related to premium setting and the accumulation of policy reserves

The Company sets insurance premiums based on the following basic calculation rates (assumed mortality rate, assumed interest rate, and assumed rate of expenses), taking into consideration the type and nature of insurance, the age and gender of the insured at the time of entering the policy, and the amount of insurance.

Assumed mortality rate Based on historical statistics, the number of deaths by gender and age is projected, and the premiums necessary to pay future insurance claims, etc. are set. The projected mortality rate used for this calculation is called the assumed mortality rate. Assumed interest rate The premiums are set by discounting a certain amount of expected return from investment of assets in advance. This discount rate is called the assumed interest rate. Assumed rate of expenses Premiums are set based on a predetermined amount of expenses required for the insurance company’s business operations. This rate is called the assumed rate of expenses. In insurance policies, if the actual mortality rate exceeds the predetermined assumed mortality rate, if the actual investment yield falls below the predetermined assumed interest rate, or if the actual expenses exceed the predetermined assumed rate of expenses, the total amount of claims and expenses to be paid will exceed the total amount of premiums and other benefits received during the insurance period, which may cause losses and affect the Group’s performance and financial position.

In accordance with the Insurance Business Act and related business regulations, the Company sets aside a significant portion of its premium income as a policy reserve for future payments of insurance claims and other benefits. Policy reserves represent the largest portion of the Company’s liabilities and are calculated based on certain assumptions regarding the frequency and timing of covered events, the amount of claims and other payments, and the amount of assets under management for each policy. If actual results deviate from these assumptions, or if future deviations are expected due to changes in the environment, an additional policy reserve may be required, which may affect the Group’s performance and financial position.

In addition, the Financial Services Agency, the financial regulator, sets regulations concerning the accumulation of policy reserves, standard interest rates and standard life tables, and any change in these factors may require a revision of premiums and additional policy reserves, which may affect the Group’s performance and financial position.

-

② Risks related to reinsurance

The Company has entered into reinsurance contracts to reduce insurance underwriting risk and asset management risk by reinsuring high-interest whole life annuity insurance policies from before privatization, in an aim to improve future earnings and capital efficiency. While we select insurance companies who meet the credit criteria set by the Company as reinsurers, and we monitor these insurance companies, if counterparty risks (the risks of reinsurance companies going bankrupt), recapture (the obligation to recover assets and risks transferred to a reinsurance company if a reinsurance contract is cancelled) risks, or asset management risks (the risks of declines in collateral asset value associated with reinsurance contracts) materialize in the future, the Group’s performance and financial position may be affected.

(2) Risks related to changes in accounting standards, tax systems, etc.

-

Deferred tax assets of the Company are recorded in accordance with current accounting standards and tax systems to the extent that future tax amounts are allowed to be reduced by the taxable income estimated based on certain assumptions. Accordingly, the Group’s business, performance, and financial position may be affected if the amount of deferred tax assets decreases due to changes in estimation assumptions resulting from a prolonged underperformance of actual results for new policies or a continued significant deterioration in the economic environment, or due to reductions in tax rates resulting from tax system reforms.

In June 2020, the International Accounting Standards Board (IASB) issued the amendments to International Financial Reporting Standards (hereinafter referred to as “IFRS”) 17, “Insurance Contracts,” which is effective for fiscal years beginning on and after January 1, 2023. Because this standard values insurance contracts at their economic value, fluctuations in each period may affect net assets. Future application of IFRS or equivalent standards in the Group’s accounting standards may affect the Group’s business, performance, and financial position.

(3) Risks related to asset management

-

Under the Medium-Term Plan, the Company will pursue portfolio restructuring with the aim of achieving sustainable growth in adjusted spread by seizing a positive turnaround in the investment environment, such as rising interest rates in Japan. We will also contribute to solving social issues and discovering core companies that will become pillars of the next-generation industries through asset management by promoting impact investment and industry-academia collaboration.

On the other hand, these asset management activities may be affected by fluctuations in domestic interest rates, foreign exchange rates, stock and real estate prices, deterioration in credit conditions, the materialization of geopolitical risks, etc., and are exposed to various asset management risks, including ① to ③ below. In preparation for such risks, the Company is working to appropriately manage assets commensurate with liabilities arising from underwriting insurance policies, and to enhance ALM (asset liability management) to stabilize profit and loss and ERM (enterprise risk management) to maintain financial soundness. In addition, we regularly conduct stress tests to verify our ability to respond to the occurrence of stress events, and we are strengthening our screening and monitoring systems, especially in the strengthening of asset management capabilities. However, if such responses are not successful, or if the market environment changes beyond expectations due to economic fluctuations in Japan or overseas or changes in monetary and fiscal policies of various countries, the Group’s performance and financial position may be affected.

-

① Market risk related to domestic interest rates

Because the Company’s asset structure has a high percentage of yen interest rate assets and the duration of the Company’s liabilities to policyholders is longer than the assets under management, the Company is exposed to the risk of fluctuations in domestic interest rates due to the mismatch between the duration of assets and liabilities.

Following the Bank of Japan’s lifting of its negative interest rate policy in March 2024, domestic interest rates have been rising, reflecting the gradual recovery of the Japanese economy and rising prices, but the situation maintains a degree of uncertainty. In this interest environment, although interest income, etc. will improve due to higher investment yields, a decline in prices of bonds already held may result in the occurrence or further growth of valuation losses, impairment losses, or losses on sales.

On the other hand, if domestic interest rates fall below current levels, we may not be able to secure the investment returns we initially expected, or we may experience a negative spread (a phenomenon in which the average investment yield of the investment portfolio is less than the assumed interest rate used to accumulate policy reserves for existing policies). In this manner, fluctuations in domestic interest rates may affect the business, performance, and financial position of the Group.

-

② Market risks other than ① above

The Company holds assets denominated in foreign currencies, some of which are hedged by forward exchange contracts, etc. However, if fluctuations in foreign exchange rates occur with respect to the portion of foreign exchange risk that has not been hedged, or even if foreign exchange risk has been hedged, if hedging costs increase due to widening interest rate differentials between Japan and overseas caused by trends in monetary and fiscal policies in various countries, and if it becomes impossible to make forward exchange contracts, etc. by rolling under the existing conditions, the Group’s performance and financial position may be affected. In addition, changes in the monetary and fiscal policies of various countries and fluctuations in foreign interest rates could cause the value of our foreign securities holdings to decline, which could affect the performance and financial position of the Group.

Furthermore, if the prices of our stock holdings decline due to the deterioration of economic or market conditions in Japan or overseas, our stock holdings may incur valuation losses, impairment losses, or losses on sales, which may affect the Group’s performance and financial position. In addition, strengthening of asset management capabilities, such as of real estate and other alternative investment management, may not produce the expected results.

-

③ Credit risks

If the financial position of the Group’s business partners, investees or borrowers, or issuers of securities held by the Company deteriorates due to changes in domestic or overseas economic trends, changes in the business environment surrounding specific industries, the occurrence of scandals, or other unforeseen circumstances, credit risk and credit-related costs may increase, or the value of our securities holdings may decline, which may affect the Group’s performance and financial position. In addition, strengthening of asset management capabilities, such as of foreign corporate and government bonds management, may not produce the expected results.

(4) Risks related to market liquidity and funding

-

① Market liquidity risk

If the Group is unable to trade financial instruments and settle funds normally in the market due to disruptions in the financial markets, or is forced to trade at prices that are significantly less favorable than usual, the Group’s business, performance, and financial position may be adversely affected. In addition, if market liquidity declines due to deterioration in domestic or overseas financial markets or economic conditions, the possibility of selling the Company’s holdings or their value may decrease.

-

② Funding risk

In the event that cash flow is tight due to an increase in payments of termination refunds following a large amount of policy surrenders and lapses or an increase in insurance claim expenditures following a significant natural disaster, and we are forced to sell assets at prices lower than the normal appraisal value to secure funds, or in the event that payment of insurance claims, etc. is delayed, it may affect the Group’s business, social credibility, performance, and financial position.

Ⅲ Business-specific

(1) Risks related to legal systems and regulations, etc.

-

① Risks related to laws and regulations under the Postal Service Privatization Act, etc.

The Company is under the supervision of the Financial Services Agency and the Ministry of Internal Affairs and Communications in accordance with the Postal Service Privatization Act and related cabinet and ministerial orders. In addition, under the Postal Service Privatization Act, the Company is subject to the opinions of the Postal Privatization Committee operated by the Headquarters for the Promotion of Privatization of the Postal Services established by the Cabinet, as well as restrictive business regulations that are not imposed on other Japanese life insurance companies (hereinafter referred to as “additional restrictions,” details stated in “I. Company Overview, 3. Details of Business, (Reference) Special Measures under the Postal Service Privatization Act” of the 20th Annual Securities Report). If these regulations further restrict our competitiveness or revenue opportunities in the future, the Group’s business may be affected.

Japan, as a member of the WTO (World Trade Organization), has established a Protocol Amending the Agreement on Government Procurement, and the rules stipulated in this Protocol are applied to institutions that have succeeded to a public corporation, accordingly, when the Company procures goods, etc., it needs to comply with the government procurement rules under the WTO. If we fail to comply with these rules through our acts or omissions, procurement actions may not be concluded, or there may be delays in procurement actions, which may prevent us from implementing the plan we originally envisioned, thereby affecting the Group’s social credibility, performance, and financial position.

-

② Risks related to the Insurance Business Act and other related business regulations

The Company is a Japanese life insurance company, and like other Japanese life insurance companies, it is subject to supervision by the Financial Services Agency under the Insurance Business Act and related business regulations. The Insurance Business Act gives the Prime Minister (delegating authority to the Commissioner of the Financial Services Agency) broad supervisory authority over the insurance business, including the authority to revoke licenses, suspend operations, collect reports, and conduct strict on-site inspections regarding matters such as accounting records. In addition, the Commissioner of the Financial Services Agency is to conduct an examination if an application for approval or notification is made regarding the establishment of a new financial product or the revision of an existing product in accordance with the said Act.

The life insurance business license is the premise of the Company’s principal business activities, and the license does not expire, and as of March 31, 2026 the Company is aware of no events that would constitute grounds for revocation of the license. However, the occurrence of such an event could have an impact on the Company’s business activities.

In addition, in the event of a problem deemed to be particularly severe from the perspectives of the soundness or appropriateness of operations based on the Insurance Business Act or other laws and regulations, etc., or a particularly serious violation of these laws and regulations, etc., the Company may be subject to administrative penalties such as orders to issue reports or improve business operations, suspension of all or part of its business operations, or revocation of its license. The Financial Services Agency has revised laws and regulations relevant to the management scheme of insurance agents, the Comprehensive Guidelines for Supervision for Insurance Companies, etc., (to be enacted on June 1, 2026, with some portions, such as revisions to guidelines for ensuring the effectiveness of guidance provided to insurance company agents, applied from August 28, 2025), and it has strengthened the management scheme for independent agents. The Company is making improvements to its systems in stages, in accordance with relevant laws and regulations, not only from the perspectives of managing agents as an insurance company (entrusting party) but also as an independent agent (entrusted party). Furthermore, if it becomes impossible to sell new products as planned in terms of content and timing, due to reasons such that the Financial Services Agency does not grant approval under the Insurance Business Act, that such approval is not granted at the timing assumed by the Company, or that the Company is not legally permitted to acquire another competitive insurance company that handles products which the Company would not be able to offer or for which it would take a large amount of time to make changes to its system to enable it to offer, or if the expected revenue cannot be secured mainly due to external factors even after such approval is granted, it may affect the Group’s performance and financial position.

The Financial Services Agency has introduced, from the end of March 2026, the economic value-based solvency regulation in line with the Insurance Capital Standard (ICS) applicable to internationally active insurance company groups, for the purpose of protecting policyholders, enhancing risk management of insurance companies, and providing information to consumers and market participants, etc. The solvency margin ratio, which is an indicator used to judge the soundness of life insurance companies, has been revised to one calculated based on this regulation from the end of the fiscal year ended March 31, 2026, and since this is a soundness indicator based on economic value, it may be significantly affected by fluctuations in the market environment.

The Company has positioned the solvency margin ratio as an important internal management indicator, and engages in management that maintains this ratio at a sufficiently high level with respect to the ratio required by the Financial Services Agency. However, if this solvency margin ratio falls below the level required by the Financial Services Agency, there is a possibility that the Prime Minister will take early corrective action, which may affect the Group’s business, performance, and financial position.

(2) Risks related to the relationship with Japan Post Co., Ltd.

-

① Risks related to provision of universal service

In order to comply with the provisions for universal service under the Postal Service Privatization Act, Japan Post Co., Ltd. has entered into a life insurance sales and maintenance agreement and a life insurance counter services agreement with the Company and is entrusted with the Company’s insurance agency business, and provides the Company’s products and services at each post office nationwide (details stated in “5. Important Contracts” of the 20th Annual Securities Report).

In particular, the life insurance counter services agreement is a contract with no fixed term and cannot be unilaterally terminated by the Company unless there are special circumstances stipulated in the contract. In addition, there is a provision in the Company’s Articles of Incorporation to the effect that the Company shall enter into a life insurance counter services agreement with Japan Post Co., Ltd., and if such agreement is terminated, an amendment to the Company’s Articles of Incorporation will be required. Accordingly, in order for the Company to terminate the life insurance counter services agreement with Japan Post Co., Ltd., it is necessary to follow these procedures and others.

Under these agreements, the Company has an obligation to maintain its status as a related insurance company in providing universal service by Japan Post Co., Ltd., and as a result, the Company’s flexible business development could become difficult.

In addition, the Group’s business, performance, and financial position may be affected by future government measures to ensure universal service, as well as amendments to laws and regulations.

Due to the enforcement of the Act to Partially Revise the Act on the Management Organization for Postal Savings and Postal Life Insurance in December 2018, of the costs required to maintain the post office network, which were previously covered by consignment commission based on contracts between Japan Post Co., Ltd., the related bank and the related insurance company(as defined under the relevant postal privatization legislation ), in accordance with the act, the essential costs for ensuring universal service (excluding the amount to be borne by Japan Post Co., Ltd.) are covered by a grant to Japan Post Co., Ltd. by the Organization for Postal Savings, Postal Life Insurance and Post Office Network (hereinafter referred to as the “Management Network”) with contributions from the related bank and the related insurance company starting from the fiscal year ended March 31, 2020.

Such essential costs constituting the basis for the calculation of the amount of contribution/grant are calculated as the sum of the following costs based on the most recent status of maintenance of the post office network.

- A. Personnel expenses, rent, construction expenses and other expenses necessary to maintain post offices, expenses necessary for transporting and managing cash, property taxes and business facility taxes, in each case, based on a post office network consisting of post offices of the minimum scale necessary to operate the network; and

- B. Expenses necessary for the minimum level of outsourcing services needed to ensure that basic postal services can be provided at contracted post offices

The contributions paid by the Company to the Management Network (57.6 billion yen paid by the Company for the fiscal year ended March 31, 2026) are the portion allocated to insurance counter operations of the total amount of such essential costs and the Management Network’s administrative costs related to the calculation of contributions and grants, which is divided proportionally between the postal counter operations, bank counter operations, and insurance counter operations, according to their expected degrees of use of the post office network.

In this manner, our contributions are calculated by the Management Network in accordance with the relevant laws and regulations, and therefore do not reflect the Company’s intentions.

As a related insurance company of Japan Post Co., Ltd. in providing universal service, we are required to make this contribution, which is a fixed operating expense unique to the Company. If the amount of such essential costs calculated by the Management Network is larger than we anticipate, the Group’s business, performance, and financial position may be affected.

-

② Risks related to consignment commission paid to Japan Post Co., Ltd.

Based on a life insurance sales and maintenance agreement and a life insurance counter services agreement, etc. signed with Japan Post Co., Ltd., as well as agent commission arrangements, etc. notified to Japan Post Co., Ltd., the Company pays consignment commission to Japan Post Co., Ltd. The commission includes those calculated by multiplying the unit cost of the services provided by Japan Post Co., Ltd. to the Company by the number of post offices, etc., and those required for the maintenance and management of policies in force, which include fixed operating expenses that are incurred independent of the volume of sales activity and may not be reduced immediately, and expenses may increase depending on work outsourced from the Company.

In addition to the above, the Company may consider introducing a commission consistent with the Group’s business strategy for each fiscal year. Failure to properly set up a consignment commission structure, including such commission, could damage the credibility of the Group, and could affect the actual result in terms of new policies or the maintenance of policies in force, as well as its business performance and financial position (details stated in “5. Important Contracts, (Reference) Consignment Commission Paid to Japan Post Co., Ltd.” of the 20th Annual Securities Report).

-

③ Risks related to the post office network and agency management

Although the majority of the Company’s products and services are provided through the post office network, recently, the diversification of means of communication has made various services necessary for daily life easily accessible via means such as the Internet, and the need for non-face-to-face services has increased. If the sales capabilities and attractiveness of the post office network are impaired due to a decrease in the number of post offices and in the number of users or the frequency of use of post offices as a result of these factors, the actual results for the number of new policies and the maintenance of the number of policies in force may be adversely affected. The Company will continue to consider and introduce means of providing products and services that complement or partially replace the post office network. However, if these measures are not successful, the Group’s business, performance, and financial position may be affected.

The Company is responsible for agency management, including the training of employees engaged in insurance counter services of Japan Post Co., Ltd., as the entrusting party under the Insurance Business Act and the life insurance solicitation and policy maintenance and operation services consignment agreement and the insurance counter services agreement concluded with Japan Post Co., Ltd. Under these circumstances, the incident involving improper use of non-public financial information and incident involving solicitation prior to obtaining regulatory approval were identified within the Japan Post Group.

The Company will deepen its understanding of the underlying causes of these incidents, ensure the effectiveness of measures to prevent recurrence, and, as the insurance company bearing responsibility for agency management, ensure the effectiveness of the agency management system in outsourcing services in general. In addition, as described in “1) Risks related to legal systems and regulations, etc., ② Risks related to the Insurance Business Act and other related business regulations,” the Financial Services Agency has amended laws and regulations concerning the insurance agency management system, and the Company is also progressively working to strengthen the system. However, in spite of these efforts, if the agency management system does not function as expected, etc., the provision of the Company’s products and services may not be carried out as expected, unexpected losses may be incurred, or administrative dispositions, etc., may be received, which may affect the Group’s social credibility, business, performance, and financial position.

(3) Risks related to the relationship with Japan Post Holdings Co., Ltd.

-

① Risks related to influence and conflicts of interest with other general shareholders due to the holding of voting rights by Japan Post Holdings Co., Ltd.

Although the percentage of the Company’s voting rights held by Japan Post Holdings Co., Ltd. is 49.7% as of March 31, 2026, Japan Post Holdings Co., Ltd. may still have influence on the outcome of resolutions of the Company’s general meeting of shareholders, such as the election and dismissal of the Company’s directors, organizational restructuring such as mergers with other companies, capital reduction, and amendments to our Articles of Incorporation.

In addition, from the perspective of the interests of the Japan Post Group,the provision of universal service, and the Japanese government’s ownership of Japan Post Holdings Co., Ltd. stock (in accordance with the Postal Service Privatization Act, the Japanese government must hold over one third of all Japan Post Holdings Co., Ltd. stocks, and as of March 31, 2026, it holds roughly 38.0% of the voting rights in Japan Post Holdings Co., Ltd.), Japan Post Holdings Co., Ltd. may exercise voting rights, etc. that are different from the interests of the Company and its general shareholders.

Furthermore, in addition to having a business contracting relationship and other transactional and contractual relationships with the Company, Japan Post Holdings Co., Ltd. has interests that differ from those of the Company’s general shareholders, such as engaging in businesses that compete or may compete with the Company through its subsidiaries, etc. (commissioned sales of products of life insurance companies other than the Company, etc.). For example, in December 2018, Japan Post Holdings Co., Ltd. entered into a basic agreement with Aflac Incorporated and Aflac Life Insurance Japan Ltd. regarding a Strategic Alliance Based on Capital Relationship. Based on this agreement, Japan Post Holdings Co., Ltd. acquired 7% (as of December 2018) of the total number of Aflac Incorporated’s common shares issued, reaffirmed its commitment to cancer insurance, and discussed new collaborative initiatives, and in June 2021, Japan Post Holdings Co., Ltd., Japan Post Co., Ltd., and the Company agreed to further develop the Strategic Alliance Based on Capital Relationship with Aflac Incorporated and Aflac Life Insurance Japan Ltd. In March 2024, Japan Post Holdings Co., Ltd. applied the equity method to Aflac Incorporated, and a portion of Aflac Incorporated’s profits is reflected in the consolidated results of Japan Post Holdings Co., Ltd. from FY2024. In addition, Japan Post Holdings Co., Ltd. entered into a business alliance agreement with Japan Post Co., Ltd. and Rakuten Group, Inc. to strengthen cooperation in various areas such as logistics, mobile, and DX in March 2021. Furthermore, in April 2021, Japan Post Holdings Co., Ltd., Japan Post Co., Ltd., Japan Post Bank Co., Ltd., and the Company signed a business alliance agreement with Rakuten Group, Inc. once again. In these agreements, Japan Post Holdings Co., Ltd. will discuss and consider collaboration in the insurance field, but the details of the collaboration may conflict with the interests of the Company and its general shareholders, such as affecting the Group’s performance.

Personal and business relationships between the Company and the Japan Post Group are as follows.

-

- a. Personal relationships with the Japan Post Group

The Company has directors who concurrently serve as directors/executive officers of the Japan Post Group, and the table below shows the main directors who concurrently serve as directors/executive officers of the Japan Post Group as of the date of submission of the 20th Annual Securities Report. In principle, except for members of the Executive Committee who concurrently serve as executive officers of the Company at the managing executive officer level or above and as executive officers of the Company who are in charge of business operations, no directors or executive officers of Japan Post Holdings Co., Ltd. attend the Company’s Executive Committee meetings. However, the Company requests representative executive officers of Japan Post Holdings Co., Ltd. to attend the meetings when we consider their attendance necessary depending on the agenda or matters to be reported.

Name Position in the

CompanyMain positions in the

Japan Post GroupReason for concurrent

appointmentTANIGAKI Kunio Director and President, CEO, Representative Executive Officer Director (part-time) of Japan Post Holdings Co., Ltd. To enhance the effectiveness of business management and management efficiency of the Group ONISHI Toru Director and Deputy President, Representative Executive Officer Managing Executive Officer (part-time) of Japan Post Holdings Co., Ltd. To respond to technical questions about the Company in the Diet as Japan Post Holdings Co., Ltd., a corporation in which the government invests more than one-third of its capital NEGISHI Kazuyuki

(Note)Director

(part-time)Director and Representative Executive Officer, President & CEO of Japan Post Holdings Co., Ltd. To strengthen Group governance scroll

(Note) He serves concurrently as a Director (part-time) of Japan Post Co., Ltd. and Japan Post Bank Co., Ltd., subsidiaries of Japan Post Holdings Co., Ltd.

The status of the Company’s directors is as described in “IV. Status of Submitting Company, 4. Corporate Governance, etc., (2) Status of Directors” of the 20th Annual Securities Report.

Although the Company accepts seconded employees and conducts personnel exchanges with Japan Post Holdings Co., Ltd., Japan Post Co., Ltd., and Japan Post Bank Co., Ltd., none of these employees holds a position that has a significant impact on the Company’s business operations.

- b. Transactions with the Japan Post Group

The Company conducts transactions with other companies belonging to the Japan Post Group, and the main transactions in the fiscal year ended March 31, 2026 are as follows.

Details of transaction Counterparty Amount

(Millions of yen)Method of determining transaction terms, etc. Payment of brand value usage fees Japan Post Holdings Co., Ltd. 1,852 As described below in “c. Brand value usage fees to Japan Post Holdings Co., Ltd.” Payment of system usage fees Japan Post Holdings Co., Ltd. 1,648 The Company, Japan Post Co., Ltd., and Japan Post Bank Co., Ltd. bear an amount calculated by multiplying the necessary expenses for providing the system by a certain profit margin ratio set in consideration of the profit margin ratio of other companies, depending on the usage of the system, etc. Payment of consignment commission for agency services Japan Post Co., Ltd. 89,830 The Company makes payments including sales commission calculated by multiplying the insurance amounts and the insurance premiums of each contract by the commission rates set for each class of insurance, and maintenance commission calculated by multiplying the unit prices set for each type of outsourcing services, such as the collection of insurance premiums and payments for insurance claims, by the number of policies in force. Postage and other charges Japan Post Co., Ltd. 5,227 Postage is charged at the same rate as general customers in accordance with our policy agreements. Lease of building owned by Japan Post Co., Ltd. Japan Post Co., Ltd. 7,154 Rent (including Common Area Maintenance charges) is set using a method similar to the cost approach for rental valuation, thereby ensuring its appropriateness. Payment of counter terminal usage fees Japan Post Bank Co., Ltd. 1,250 The Company and Japan Post Bank Co., Ltd. set the share according to the number of terminal operations handled, and the Company pays an amount corresponding to its share of the maintenance costs of the counter terminals. scroll

(Note) In addition to the above, as described in “III Business-specific, (2) Risks related to the relationship with Japan Post Co., Ltd., ① Risks related to provision of universal service,” there was a payment of 57.6 billion yen in the fiscal year ended March 31, 2026 for contributions to the Management Network in relation to the maintenance of the post office network.

In order to ensure the appropriateness of transaction terms with other companies belonging to the Japan Post Group, the Company has established a system whereby resolutions are passed at meetings of the Board of Directors, including outside directors, when new important transactions are implemented, or existing important transaction terms are changed.

- a. Personal relationships with the Japan Post Group

-

② Risks related to brand value usage fees to Japan Post Holdings Co., Ltd.

As stated in “5. Important Contracts” of the 20th Annual Securities Report, the Company has concluded the Japan Post Group Agreement and other agreements with each company in the Japan Post Group, and matters necessary for the appropriate and smooth operation of the Group or matters requiring management by Japan Post Holdings Co., Ltd. under laws and regulations are subject to prior consultation with Japan Post Holdings Co., Ltd. or reporting to Japan Post Holdings Co., Ltd. In addition, the Company is licensed by Japan Post Holdings Co., Ltd. to use “Kampo Seimei” and other trademarks, and pays brand value usage fees to Japan Post Holdings Co., Ltd. as consideration for the benefit of being able to utilize the brand power of the Japan Post Group in the Company’s business activities.

Based on the concept that the brand value we derive from belonging to the Japan Post Group is reflected in our business performance, this fee is calculated by multiplying the amount of insurance policies in force as of March 31, 2025, a performance indicator that reflects such benefit, by a certain rate (0.0036%), and this rate will not be changed unless there is a significant change in economic conditions or other special circumstances. The brand value usage fees will continue to be paid as long as the Company belongs to the Japan Post Group, and the obligation to pay such royalty fees will continue as long as the Company operates as a related insurance company as defined in the Act on Japan Post Co., Ltd., regardless of the percentage of the Company’s shares held by Japan Post Holdings Co., Ltd.

If the Company is no longer able to use the trademark under the conditions as of March 31, 2026 due to the termination or revision of these agreements, etc., or if the calculation method of brand value usage fees is changed due to significant changes in economic conditions or other special circumstances, the Group’s business, performance, and financial position may be affected.

-

③ Risks related to additional disposal of the Company’s shares by Japan Post Holdings Co., Ltd.

As described in “III Business-specific, (3) Risks related to the relationship with Japan Post Holdings Co., Ltd., ① Risks related to influence and conflicts of interest with other general shareholders due to the holding of voting rights by Japan Post Holdings Co., Ltd.,” while the percentage of the Company’s voting rights held by Japan Post Holdings Co., Ltd. is 49.7% as of March 31, 2026 under the Postal Service Privatization Act, Japan Post Holdings Co., Ltd. aims to dispose of all of the Company’s shares held by Japan Post Holdings Co., Ltd. as soon as possible, taking into consideration the Company’s business situation and the impact on the provision of universal service. However, as of the filing date of the 20th Annual Securities Report, a bill to revise the Postal Service Privatization Act, including provisions concerning the disposal of the Company’s shares, has been submitted to the Diet. Even amid these circumstances, Japan Post Holdings Co., Ltd. has announced that it will continue to consider the disposal of the Company’s shares, taking into account the purpose of the Postal Service Privatization Act and the perspective of Japan Post Group management.

In accordance with the Postal Service Privatization Act, the Company is subject to additional restrictions that other companies in the industry are not. However, such restrictions will cease to apply when (i) Japan Post Holdings Co., Ltd. disposes of all of its shares in the Company, or (ii) Japan Post Holdings Co., Ltd. disposes of one-half or more of its shares in the Company, and the Prime Minister and the Minister of Internal Affairs and Communications recognize that there is no risk of impeding appropriate competitive relationships with other financial institutions and appropriate provision of services to users and determine that the additional restrictions do not apply to the Company. As of March 31, 2026, the percentage of the Company’s shares held by Japan Post Holdings Co., Ltd. is below 50%, and Japan Post Holdings Co., Ltd. has notified the Minister of Internal Affairs and Communications that it has disposed of more than one-half of the Company’s shares. However, as of the present date, the decision regarding (ii) above has not been made and it is unclear when and how the additional restrictions will be removed. Under such circumstances, if the sale of our shares by Japan Post Holdings Co., Ltd. does not proceed, the removal of the additional restrictions may not take place, and the expanded management flexibility that Japan Post Holdings Co., Ltd. and the Company expect may not be realized. On the other hand, if additional sales of our shares are made by Japan Post Holdings Co., Ltd. in the future, or if there is a widespread perception in the market that such sales will increase the number of our shares circulating in the market and worsen the supply-demand balance, the liquidity of the Company’s shares and the formation of the Company’s stock price may be affected.

In addition, if the terms and conditions of the life insurance solicitation and policy maintenance operations consignment agreement, the insurance counter operations agreement, or any other agreements that the Company has concluded with Japan Post Co., Ltd. are changed to the Company’s disadvantage or if such agreements are terminated as a result of the sale of the Company’s shares by Japan Post Holdings Co., Ltd., a large amount of cost, time, etc. may be required to maintain our business as before due to such factors as inability to use the post office network, which may affect the Group’s business, performance, and financial position. In addition, with respect to the Japan Post Group Agreement and the Japan Post Group Trademark Management Agreement that the Company has concluded with the Japan Post Group, as well as the Agreement Relating Japan Post Group Management and the Group Trademark Management Agreement that the Company has concluded with Japan Post Holdings Co., Ltd., if the Company ceases to be a related insurance company and an agreement or contract itself is not applied, the Group’s business, performance, and financial position may be affected.

Furthermore, although the Company has not received any guarantee or other credit enhancement from the Japanese government or any other public institution, in the event that the misconception or illusion that the Company’s economic creditworthiness has declined is widely propagated in society as a result of Japan Post Holdings Co., Ltd. ceasing to be the Company’s parent company, this could have a negative impact on employee recruitment activities, induce customers and other business partners to suspend transactions, reduce transaction volume, cancel insurance contracts, or change terms and conditions of transactions to those that are unfavorable to the Company.

Ⅳ Operation

(1) Compliance risk and operational risk management

-

The risk of compliance violations and operational risk exist in the course of the Group’s business operations and may include internal and external illegal activities or misconduct, occurrence of problems in labor management and workplace environment, loss of credibility due to inadequate response to customer-first business operations, business interruption due to system failure, etc., inappropriate business operations, inadequate payment of insurance claims and other payments, pressures on operation systems, inadequate trademark applications and other operations, deficiencies in the management of agents, contractual violations and other problems caused by outsourcing operations. In particular, because most of the Company’s products and services are provided through the post office network, where not only our business but also banking and logistics services are provided in parallel, the possibility of these operational risks materializing is relatively high, which may affect our business, social credibility, performance, and financial position.

-

① Risks related to compliance

The Group is under the supervision of the Financial Services Agency and the Ministry of Internal Affairs and Communications in accordance with the Insurance Business Act and the Postal Service Privatization Act. In addition, as a business that handles life insurance policies, the Group is obligated to comply with various related laws and regulations, including the Insurance Act, the Consumer Contract Act, the Act on the Protection of Personal Information, and the Act on Prevention of Transfer of Criminal Proceeds, and has established a Compliance Program up until now to ensure compliance with laws and regulations through regular compliance training for executives and employees, thorough information management, and strengthening of measures against crime prevention, anti-money laundering, combating the financing of terrorism, and countering proliferation financing. However, the occurrence of violations of laws and regulations due to acts or omissions by executives or employees, or the ineffectiveness of measures taken to prevent violations of laws and regulations, may affect the social credibility and business of the Group. In addition, although the Company has entered into a vast number of insurance policies and contracts for operations consignment and purchase of goods, in the event that the Company is the victim of fraudulent acts by the other party to the contract, or if it enters into a contract with antisocial forces, the social credibility and business of the Group may be affected. Furthermore, the Group is exposed to the risk of potential losses due to fraud and other forms of misconduct by its employees, agents, contractors, and policyholders. The Company’s employees and agents hold personal information of policyholders through their interactions with policyholders, and there is a possibility that illegal sales techniques, fraud, identity theft, loss or leakage of personal information, or inappropriate use of such information may occur. Although we take measures to prevent or detect such illegal activities, if our initiatives fail to eliminate them, the social credibility and business of the Group may be affected.

In this manner, the Group is subject to various regulations such as the Insurance Act and the Act on Prevention of Transfer of Criminal Proceeds, and any revision of such regulations or change in government policy regarding their enforcement may result in new responses, costs, etc., which may affect the Group’s business, performance, and financial position.

-

② Conduct risks

Based on our reflection on the solicitation quality issues, etc., the Group defines the risk of losing the trust of customers and other stakeholders due to acts that violate social expectations, such as acts that lack the user perspective, as well as compliance with laws and regulations, resulting in damage to corporate value, as conduct risk, and has designated the compliance department as the overseeing department to establish and strengthen the company-wide risk management system. Through these initiatives, we will detect risk information with a high level of risk sensitivity and instill in each employee the behavior that meets society’s expectations, thereby curbing the manifestation of conduct risks in the insurance solicitation process and in all other business operations.